COREDO – EU Legal & Compliance Services Expert legal consulting, financial licensing (EMI, PSP, CASP under MiCA), and AML/CFT compliance across the European Union. Headquartered in Prague, we provide seamless regulatory solutions in Germany, Poland, Lithuania, and all 27 EU member states.

Pavel Kos

22.02.2026 | 6 min read

Updated: 22.02.2026

I have been leading COREDO since 2016 and often see strong products stall in Latin America because of two factors: choosing the wrong acquiring model and underestimating local regulatory and technical nuances. The COREDO team has implemented dozens of projects in the EU, the UK, Singapore and Dubai, and in recent years: in Brazil and Mexico. This has allowed us to develop tools that shorten time-to-market, lower MDR and increase authorization rate without compromises on compliance.

In this article I have compiled operational best practices for e‑commerce, marketplaces, fintech companies and subscription services. The text is both strategic and applied: from choosing a model (local vs international acquiring) to specific KPIs, fraud rules, onboarding checklists and our migration practice from foreign PSPs to local acquirers.

Local acquiring in Latin America

Latin America: one of the fastest-growing online payments markets, and acquiring in Latin America requires local thinking. Card acquiring in Brazil and card acquiring in Mexico work differently than in Europe or Asia: a strong role of local schemes (ELO, Hipercard), alternative methods (Pix, Boleto, Oxxo Pay) and the specifics of address scoring.

International acquiring Brazil/Mexico is attractive for its ease of getting started, but often loses conversion: issuing banks in LATAM are more likely to decline cross-border transactions. In e-commerce this hits the authorization rate and raises the decline rate without objective reasons. COREDO’s practice confirms: local routing and local payment methods deliver a conversion increase of 10–25% compared with pure cross-border.

Acquiring: local vs international

The choice between local and international acquiring directly affects conversion, MDR level and the risk of encountering hidden fees. Let’s look at the advantages local acquiring provides in Brazil and how that is reflected in the final price and decline rates.

Acquiring in Brazil: advantages

Local acquiring in Brazil provides direct access to ELO and Hipercard, support for installments (parcelado) and precise risk scoring taking into account ZIP codes and device fingerprinting. A solution developed at COREDO for a fashion retailer showed an approval rate increase from 67% to 86% after switching to local processors Cielo and Rede, taking into account EMV 3‑D Secure 2 (3DS2) and tokenization.

With local acquiring it’s easier to connect Pix and Boleto bancário, which covers the “cash” segment and customers without cards. This is especially important in regions and the suburbs, where card penetration is lower and the share of Pix and Boleto is higher than in megacities.

Advantages of local acquiring in Mexico

In Mexico, local acquiring increases card approvals by taking into account Banxico rules and local behavioral analytics. Integration with PSPs in Mexico allows adding Oxxo Pay and SPEI/CoDi, which provides a noticeable uplift in conversion for marketplaces and digital services.

For offline, POS acquiring and terminals in Mexico are no less important than the online channel: support for EMV, contactless and NFC is better validated through a pilot in two or three states: authorization dynamics outside the city and in the capital differ. Our experience at COREDO showed that calibrating fraud rules by region reduces the false positive rate by 15–20%.

MDR and hidden fees: where percentages are lost

MDR fees in Brazil and MDR fees in Mexico depend on MCC, average ticket, chargeback profile and local payment methods. In Brazil, parcelado increases the total cost of ownership of acquiring due to financing of installments. In Mexico, cash via Oxxo Pay adds fixed fees.

Hidden acquiring fees in Latin America are often hidden in FX conversion (BRL/MXN to USD), fees for early settlement (T+0) and additional percentages for high‑risk MCCs. The COREDO team usually requests a full breakdown of unit economics: interchange, scheme fees, acquiring markup, rolling reserve, collateral and settlement fees, to avoid surprises and correctly calculate ROI.

Conversion: local/international

The comparison of local and international acquiring by conversion is almost always in favor of local. Authorization rate in Brazil and Mexico increases due to:

- local routing to Cielo, Rede, Getnet, PagSeguro;

- support for local schemes (ELO/Hipercard);

- 3DS2 according to issuers’ regional rules and soft declines retry logic.

On one project the decline rate fell from 24% to 11% after implementing re‑processing and retry logic with local timeouts. This is a case where upgrading scoring and routing produced a noticeable effect without a sharp increase in fraud.

Regulation and Licensing

An analysis of the regulatory framework and licensing requirements shows which legal and operational standards govern the work of financial institutions across different jurisdictions. The section sequentially examines practical examples and regulatory reporting, in particular the approach of the Banco Central do Brasil and the specifics of Brazilian supervision.

Central Bank of Brazil Reporting

Acquiring regulator: Banco Central do Brasil. For payment service providers and acquirers a licensing and reporting regime applies, including capital requirements, risk management and information security. A separate layer is LGPD as the basis for data privacy and data localization.

KYC/AML requirements for merchants in Brazil include CDD, PEP screening and ongoing transaction monitoring. Suspicious transactions are reported through channels established by the regulator (local equivalents of SAR) involving COAF. In COREDO projects we embed these flows at the process design stage to avoid revisiting the architecture months later.

Banxico and CNBV in Mexico

In Mexico supervision is carried out by Banco de México (Banxico) and CNBV (Comisión Nacional Bancaria y de Valores). Regulatory requirements for acquiring in Mexico cover operational risks, PLD/FT (AML/CFT) and transaction reporting rules. For marketplaces it is important to understand the status of split settlements and the procedure for disclosing fees in statements.

KYC/AML requirements for merchants in Mexico involve identification of beneficiaries, PEP screening and automation of anomaly monitoring. Local “SAR-like” notifications are processed through national mechanisms in cooperation with financial institutions. Implementing the correct onboarding questionnaire and document checking at an early stage saves weeks during submission.

Local Registrations and Taxation

To enter the Brazilian market, a foreign seller often needs to open a CNPJ and a local legal entity, especially when using local acquiring and working with Pix/Boleto. Taxation of payments in Brazil for non-residents affects service taxes and possible withholding tax, and this needs to be modeled in advance.

In Mexico, obtaining an MX RFC often becomes a mandatory step for local settlements and issuing fiscal documents. Taxation of payments in Mexico for foreign sellers includes IVA and local withholdings for certain delivery models. At COREDO we work together with tax advisors to build a cascade of contracts and settlement flows to avoid double taxation and mismatches between VAT/IVA.

Impact of payment methods on strategy

Payment methods shape a company’s commercial and operational decisions, defining the customer experience, risks and monetization channels. Understanding their impact on strategy is especially important when assessing local innovations, for example how Pix is changing card acquiring in Brazil.

How Pix affects acquiring in Brazil

Pix: Brazil’s instant payments that changed basket composition. In low AOV categories Pix pulls share from cards, lowering the MDR, but changing decline and return behavior. In high‑ticket segments cards and parcelado still dominate, and card acquiring in Brazil remains critical.

COREDO’s practice confirms: the optimal strategy is hybrid. Pix is used as the primary offer for price‑sensitive buyers, but cards retain priority for subscriptions and installments. It’s important to set up reconciliation for Pix and cards in a single register.

Why connect Boleto, Oxxo and CoDi/SPEI?

Boleto bancário – a bank payment with delayed confirmation. It increases conversion in regions and among customers without cards, but requires careful inventory management due to confirmation delays.

In Mexico the role of CoDi (Cobro Digital) and SPEI is in instant transfers, and Oxxo Pay covers cash scenarios. Connecting local payment methods (Boleto, Oxxo Pay, Pix) expands the audience, but increases the complexity of reconciliation and risk rules. The solution developed by COREDO for a marketplace in Mexico combined CoDi/SPEI and cards into a single settlement calendar and reduced operational errors in reconciliation statements by 40%.

Processors and local schemes

Support for ELO, Mastercard, Visa, Hipercard in Brazil is mandatory. Among local processors we most often see Cielo, Rede, Getnet and PagSeguro; their behavior in terms of authorization rate differs from MCC to MCC. Correct routing between acquirer processor via ISO 8583 and, where available, ISO 20022, yields an increase in approvals and resilience.

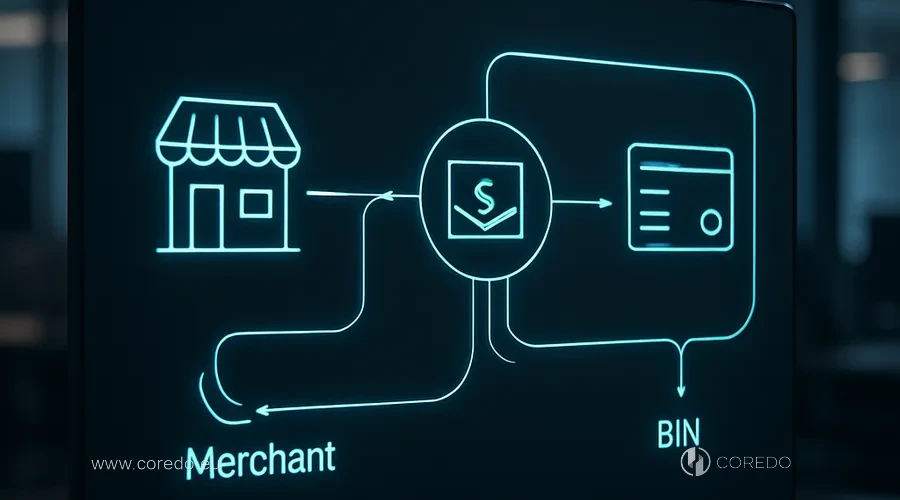

Connection models: Merchant/PayFac/BIN

The choice of connection model — classic merchant, PayFac or BIN sponsorship — is determined by a combination of requirements for control, speed to market and operational responsibility. This determines how quickly and legally a European business can connect acquiring in Brazil, which legal and technical requirements will need to be met, and what costs will arise.

How to connect acquiring in Brazil

For a European merchant, the question “how to connect acquiring in Brazil for a European business” starts with choosing a model: a local company with a CNPJ and a local merchant account, or an international PSP with local routing. The first option takes more time but delivers the best conversion and control over MDR.

How long does it take to open a merchant account in Brazil? In COREDO’s practice — from 3 to 6 weeks for low-/mid-risk with ready PCI DSS infrastructure and transparent KYC. High-risk, installment plans and marketplace models extend the timeframe to 8–10 weeks due to underwriting and fraud testing.

Acquisitions in Mexico by a foreign company

In Mexico, “how to connect acquiring in Mexico for a foreign company” depends on having an RFC and a local bank account for settlements in MXN. Without local presence, a hybrid approach is reasonable: an international provider with a local partner and integration with Oxxo/SPEI.

How long does it take to open a merchant account in Mexico? On average 2–5 weeks for standard categories and up to 7–9 weeks for marketplaces with split settlements, when deeper Due Diligence of sub-merchants is required.

PayFac and BIN sponsorship in Latin America

The PayFac model vs a classic merchant account in LatAm is a question of scale and control. PayFac/aggregator simplifies onboarding of sub-merchants, speeds up go-live and provides ready white-label acquiring. A classic merchant account increases margin and flexibility of risk policies, but requires its own license/registration and processes.

BIN sponsorship in Latin America is becoming sought after by those building their own payment products or cards. At COREDO we support negotiations with sponsoring banks, design compliance and help to pass technical certification to shorten the path from MVP to pilot.

Underwriting: reserves and holdbacks

Underwriting and merchant due diligence in LatAm are based on MCC, AOV, CBR and chargeback history. Rolling reserves and acquiring reserves in LatAm are applied more often in high-risk and subscription models. The clearer the KYC package and refund policy, the lower the collateral and the faster the holdbacks are released.

API, PCI, EMV 3-D Secure: security

A reliable technical and security foundation is not a set of abstract requirements but a practical toolkit: APIs, PCI compliance, implementation of EMV 3‑D Secure and tokenization provide security and trust during transactions. When integrating for marketplaces and mobile applications, the correct combination of these components ensures both regulatory compliance and convenience for users.

Marketplace and application integration

Technical integration of acquiring APIs for marketplaces requires support for marketplace payments and split settlements at the acquirer/PSP level. Online for Brazil: online acquiring for marketplaces with support for parcelado, Pix and local schemes; for Mexico: compatibility with Oxxo and SPEI is required.

If the question is “how to choose an acquirer for a mobile app in Brazil”, I look at the SDK, stability of mobile 3DS2, tokenization and offline modes for contactless. Payment page conversion and UX metrics directly affect unit economics and approval cost.

PCI DSS, EMV and tokenization

PCI DSS and local compatibility for acquiring: the foundation. We determine the SAQ type, deploy P2PE on terminals and encrypt PAN on entry. EMV and contact/contactless payments in Latin America create a liability shift: in the absence of EMV, fraud liability falls on the party without EMV support.

EMV 3‑D Secure and 3DS2 for LATAM increase security and approval rate when friction is configured correctly. Tokenization and PAN tokens reduce fraud and improve UX, especially in recurring payments and apps with one‑click purchases.

Fraud management: reducing declines

Fraud management and transaction profiling are built on a combination of rules and machine learning for fraud detection. We use fraud indicators: BIN analysis, velocity rules, device fingerprinting and geo-patterns. The balance between protection and conversion is expressed in the false positive rate: reducing it directly increases revenue.

How to reduce declines in Brazil and Mexico: apply local BIN tables, multi-step retry on soft declines, correct MCCs and specialized routing by card types. Re‑processing helps recover up to 5–8% of declined attempts with proper timeouts and limits.

Operational processes: settlements and FX

In operational processes, settlements, FX management, timely reporting and regular reconciliation play a key role – the accuracy and transparency of financial flows depend on them. Particular attention is required for settlement cycles and settlement timelines, since their configuration determines how quickly and correctly positions will be closed and reports generated.

Settlement cycles: settlement timelines

Settlement cycles and settlement timelines in Brazil and Mexico vary by payment methods and providers. Cards are more often T+1/T+2, Pix and SPEI: closer to T+0/T+1, while Boleto and Oxxo have confirmation delays. Settlement lag is critical for cash‑flow: the financial model must account for schedules and possible holds.

Hedging currency settlements

FX and currency conversion in international payouts (BRL, MXN, USD) are a zone of hidden losses. Settlement currency and FX spread affect the final MDR when converted to the base currency. We set control rates, use hedging and verify chains of international transfers and correspondent banks so as not to lose margin in transit.

Data privacy and GDPR for European companies in LATAM require special attention to data localization and storage requirements. I recommend determining in advance which personal data fields are stored in the EU, and which are in Brazil/Mexico taking into account LGPD and the local regime.

Reporting, MCC and AML monitoring

Reporting requirements to Banco Central do Brasil and Banxico include operational and statistical data, as well as specific forms on payment flows. MCC and risk categorization affect limits, escalation thresholds and chargeback thresholds. A merchant registry and AML monitoring must be regularly updated: this helps pass independent audits without emergencies.

Reconciliation and accounting for cross‑border sales we build taking into account splits, refunds, chargebacks and multi‑currency reporting. Such a stack frees the CFO from manual reconciliation and reduces errors in P&L.

Chargebacks and disputes: rules and metrics

Managing chargebacks and disputes requires clear rules and precise metrics to effectively reduce losses. Below we will examine key procedures, including representment stages, and practical steps to decrease the number of disputed transactions.

Representment procedures

Chargebacks and disputes in Latin America are subject to card scheme rules, but local issuers add nuances. Chargeback and representment rules require careful documentation: proof of delivery, authorization logs, 3DS results and the history of communication with the customer.

Chargeback to sales ratio (CBR) and chargeback thresholds, key benchmarks for risk teams. When CBR increases acquirers build up reserves and may change fees. Our team configures alerts and a weekly root-cause analysis to act proactively.

Reducing chargebacks and declines

How to reduce the chargeback rate in Latin America? Combine a clear returns policy, local customer support, correct descriptors and 3DS2 with adaptive friction. For subscriptions: proactive notifications and token updates reduce disputed charges.

KPI: approval rate, average ticket and chargeback rate should be visible on a single dashboard. Decline rate analysis and soft declines combined with retry logic provide quick wins while the main fraud strategy “learns” on new data.

Subscriptions and recurring payments

acquiring services for subscriptions and recurring payments in Mexico and Brazil require stable tokenization and card update models. AOV, LTV and CAC are metrics that directly depend on the unit economics of the transaction and the cost of approval. Smart routing and local tokens reduce churn caused by declines.

COREDO case studies: what worked

COREDO case studies show what worked in practice across different markets and challenges. Below: real examples, including cost reductions and ROI growth in Brazil, with an analysis of the approaches used and results achieved.

Cost reduction and ROI growth in Brazil

One of COREDO’s projects, a digital service with international acquiring in Brazil, had a high decline rate and MDR. After migrating to a local acquirer and adding Pix the overall cost per approval fell by 18%, ROI on implementing local acquiring paid back in 4.5 months, and the approval rate increased by 17 percentage points. The ROI estimate when switching to local acquiring was based on real AOV, MDR, chargebacks and settlement lag data.

Checklist for migrating from a foreign PSP

Migration from a foreign PSP to a local acquirer – a checklist that the COREDO team uses regularly:

- audit of MDR and all markups, including FX and early settlement;

- comparison of authorization rates by BIN and MCC;

- verification of 3DS2 flow and tokenization;

- setting up split settlements and marketplace payouts;

- tests of re-processing and retry logic on soft declines;

- legal section: contracts, KYC, rolling reserve, SLA for disputes.

We carry out PSP integration in Brazil and PSP integration in Mexico taking into account processing technology stacks: ISO 8583 gateways, webhooks, idempotency keys and reporting. This reduces downtime risk when switching traffic.

Choosing a partner by region

M&A and due diligence when choosing an acquiring partner include checking licenses, reserves, SLAs and the 3DS/EMV roadmap. White‑label and SaaS acquiring solutions are suitable for fintech companies and marketplaces seeking to control UX without their own acquiring license.

Regional differences “city vs province” in card acceptance are noticeable: in metropolises there’s a higher share of contactless and 3DS approvals, in regions, a greater weight of Pix/Oxxo and sensitivity to timeouts. We take these observations into account in routing and scoring.

Step-by-step roadmap

Step-by-step recommendations and action plans will help structure entry into the Brazilian market and avoid common mistakes when setting up acquiring. Below is a checklist for European businesses with specific steps on legal requirements, provider selection, and integrating payment solutions in Brazil.

How to set up acquiring in Brazil

- Legal structure: assessing the need to open a CNPJ and a local account.

- Licensing/partnership: choosing a local acquirer/PSP (Cielo, Rede, Getnet, PagSeguro) and setting up a merchant account and merchant ID.

- Payment methods: cards (including ELO/Hipercard), Pix, Boleto; EMV 3DS2.

- Security: PCI DSS (SAQ scope determination), P2PE, tokenization, EMV liability shift control.

- Technology: API/SDK, ISO 8583 compatibility, fallback routing, retry logic.

- Risk: fraud rules, ML model, BIN analysis, velocity rules.

- Operations: settlement cycles (T+1/T+2), rolling reserve, reconciliation and reporting in regulator format.

- Taxes: VAT/IVA impact, withholdings, FX strategy for BRL/USD and hedging.

How to set up acquiring in Mexico

- Registration: assessing the need for an MX RFC and a local bank account.

- Partnership: choosing an acquirer/PSP that supports Oxxo Pay, SPEI/CoDi and 3DS2.

- Model: PayFac/aggregator vs classic merchant with white-label capabilities.

- Technology: marketplace payments, split settlements, webhooks, idempotency.

- Security: PCI DSS, SAQ, EMV contact/contactless, tokenization.

- Risk: chargeback and representment rules, chargeback thresholds, monitoring.

- Operations: settlement currency (MXN/USD), FX conversion, correspondent banks.

- Reporting: Banxico/CNBV requirements, merchant registry, AML monitoring and local suspicious activity notifications.

Acquiring as a growth driver, not a cost

Acquiring for e‑commerce in Latin America: it’s about strategy, architecture and execution discipline. In Brazil and Mexico the advantage comes from local acquiring with support for alternative methods, correct routing, a strong fraud stack and a transparent operating model with control of FX and settlement cycles. When all elements converge, authorization rate grows, MDR decreases relative to revenue, and chargeback risk remains manageable.

COREDO accompanies clients throughout the entire journey: from registering a company abroad, obtaining financial licenses and AML consulting to integrations with acquirers, building a PayFac model and BIN sponsorship. I see my role as shortening your path to the LATAM market, removing regulatory and technical barriers and turning payments into a sustainable competitive advantage. If you are planning a launch in Brazil or Mexico – we’ll discuss your funnel, KPIs and risks and put together a realistic roadmap with clear timelines and budget.